Index

The U.S. matcha boom isn’t over. If anything, it’s getting more complex. More than 90 million annual searches tell a story not of a fading trend, but of a market diversifying in how it’s consumed and what consumers are looking for—some reaching for a latte, others hunting down ceremonial grade powder, others experimenting with recipes at home. The word “matcha” covers all of it, but what people want from it is increasingly different.

This article unpacks the U.S. matcha market through search data: how large it’s grown, what’s driving each format, and what shifting search paths signal about where consumer demand is heading next.

The U.S. Matcha Market: Scale, Growth, and What’s Changing

By search volume, the U.S. matcha market has expanded significantly in both scale and depth.

Market size (ListeningMind, June 2022–May 2026):

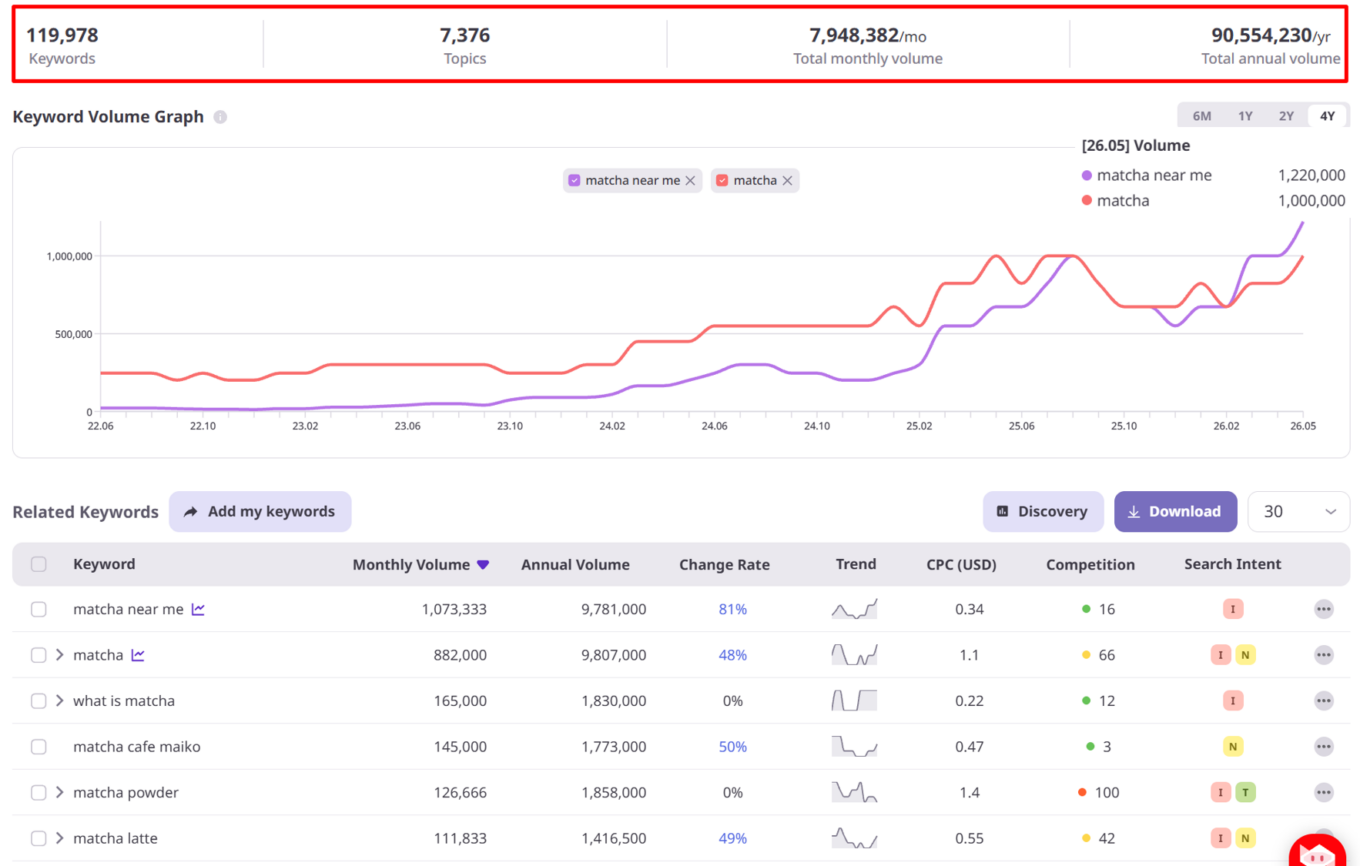

- Keywords: 119,978

- Total monthly search volume: 7,948,382

- Total annual search volume: 90,554,230

The most telling shift isn’t in total volume alone—it’s in the pace of change. The broad term

matcha

has climbed to 882,000 monthly searches, and

matcha near me

has surged to over 1,073,000—now the highest-volume keyword in the category.

Also worth noting:

matcha near me

crossing the 1,073,000 mark is a sign that matcha is no longer just an online purchase decision. Consumers are actively seeking out cafés and stores where they can experience it in person.

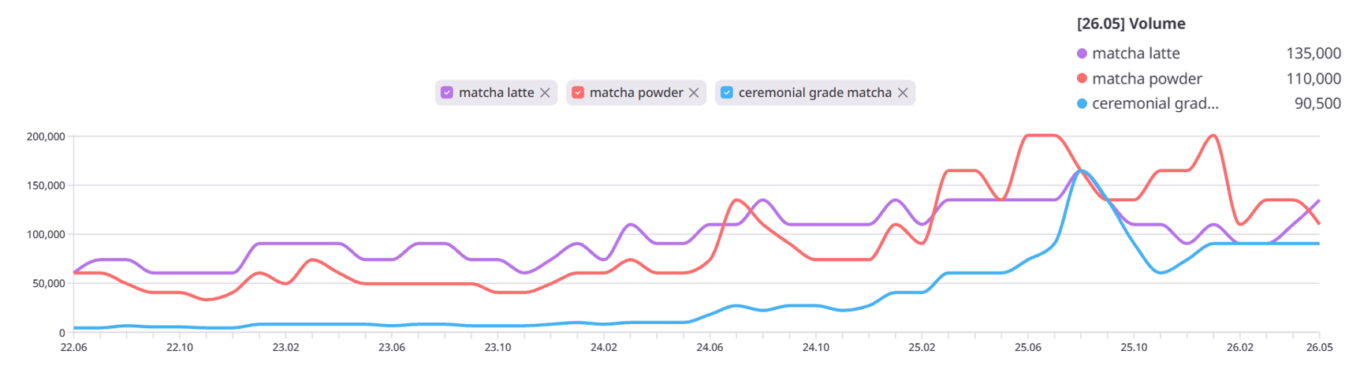

Matcha Powder vs Matcha Latte vs Ceremonial Grade Matcha: Which Format Is Growing?

Each of the three major formats is growing differently—and playing a different role in the market.

matcha powder

,

matcha latte

, and

ceremonial grade matcha

Matcha latte — steady, structural growth

Monthly: 111,833 / Annual: 1,416,500.

Since 2022, matcha latte has shown consistent year-over-year growth, with each new baseline sitting higher than the last. Its strong associations with Starbucks and Dunkin suggest it continues to serve as the primary entry point into the matcha category for many American consumers.

Matcha powder — largest volume, growth moderating

Monthly: 126,666 / Annual: 1,858,000.

Matcha powder remains the highest-volume format of the three. However, growth momentum has slowed, likely reflecting a combination of demand stabilizing in the latte segment and consumers redistributing interest toward ceremonial grade. The floor remains high; the ceiling has likely been reached for now.

Ceremonial grade matcha — near-vertical surge

Monthly: 90,500 / Annual: 1,112,000.

From roughly 4,400 monthly searches in 2022 to a peak of 165,000 in August 2025—approximately 37x growth in four years. This kind of near-vertical surge typically reflects a wave of informed newcomers entering a category quickly. Ceremonial grade matcha is now approaching the search volume of latte and powder, and may well become the dominant format in the coming years.

Notably, all three formats saw simultaneous volume increases in the second half of 2024 through 2025. This wasn’t a single-format story—the broader matcha boom appears to have lifted the entire market.

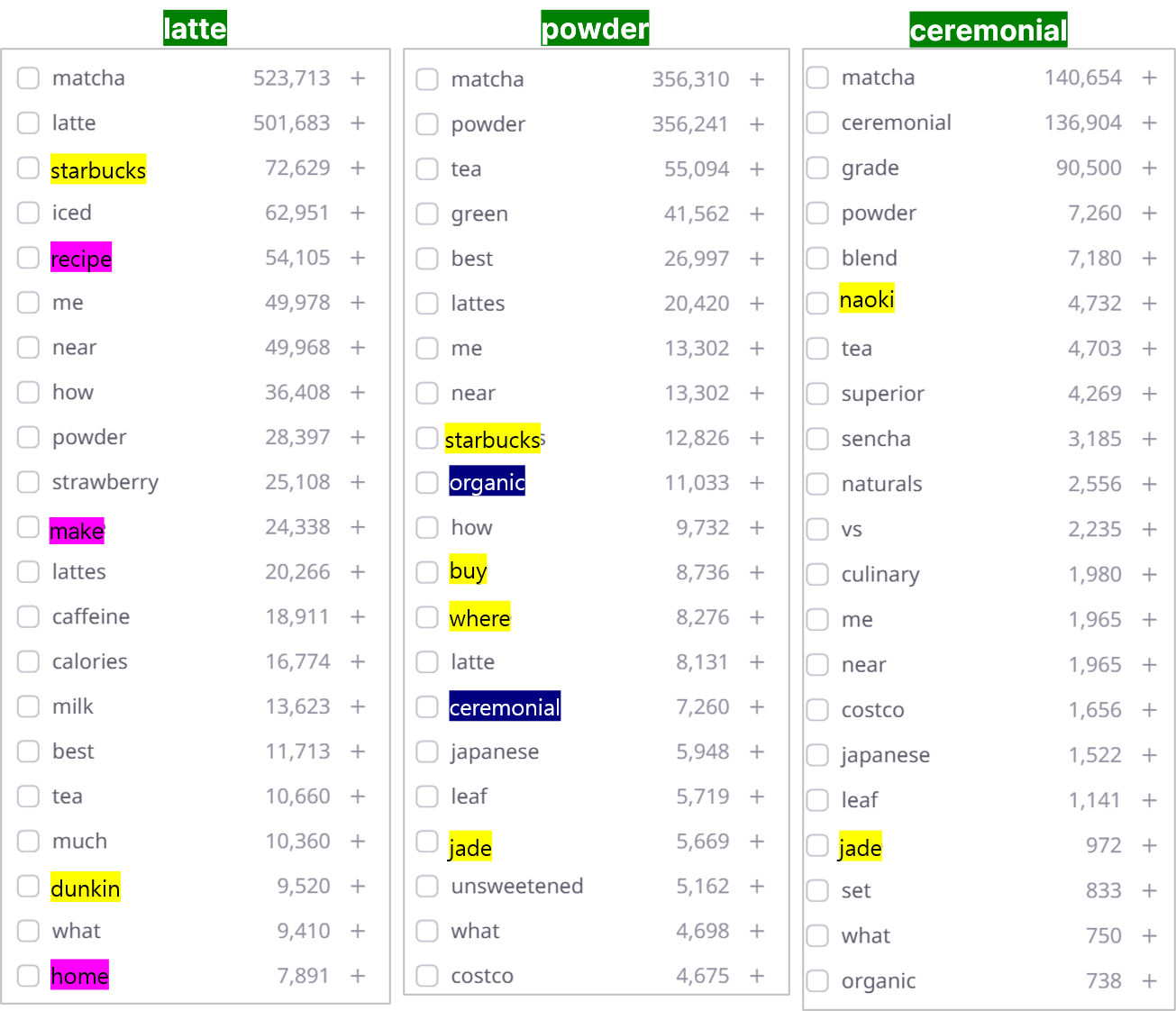

What Are People Actually Searching for in Each Matcha Format?

Topic data reveals that each format is drawing in a distinctly different type of consumer.

Matcha latte: experience and recipe-driven Search topics split evenly between in-store discovery (

starbucks

,

dunkin

,

near me

) and at-home recreation (

recipe

,

make

,

home

,

how

). The pattern suggests a consumer journey that starts at the café and moves toward DIY. Variation-focused topics like

strawberry

and

iced

round out a picture of a format that rewards customization and creativity.

Matcha powder: purchase-intent traffic Top topics include

starbucks

,

buy

, and

where

—signals of a large population in active purchase consideration mode. Notably,

ceremonial

,

organic

, and

jade

also appear in the top 20, suggesting that powder searchers are already beginning to factor in grade and quality. This format attracts consumers who are ready to buy, but still figuring out what to buy.

Ceremonial grade matcha: brand selection by informed buyers Topics like

vs

,

culinary

,

blend

, and

sencha

dominate—language that signals consumers who are comparing products with a working knowledge of the category. Japanese brand names including

naoki

and

jade

appear alongside quality and production-related terms, reflecting a population actively weighing their options rather than searching for a starting point.

A pattern across formats One structural difference worth flagging: for matcha latte and matcha powder,

starbucks

appears consistently in the top topics—functioning as a reference point and comparison anchor for those formats. For ceremonial grade matcha, the reference points shift entirely to Japanese brands like

naoki

and

jade

. Latte and powder consumers are navigating the matcha market through the lens of American café culture; ceremonial grade consumers are navigating it through the lens of Japanese sourcing and quality standards.

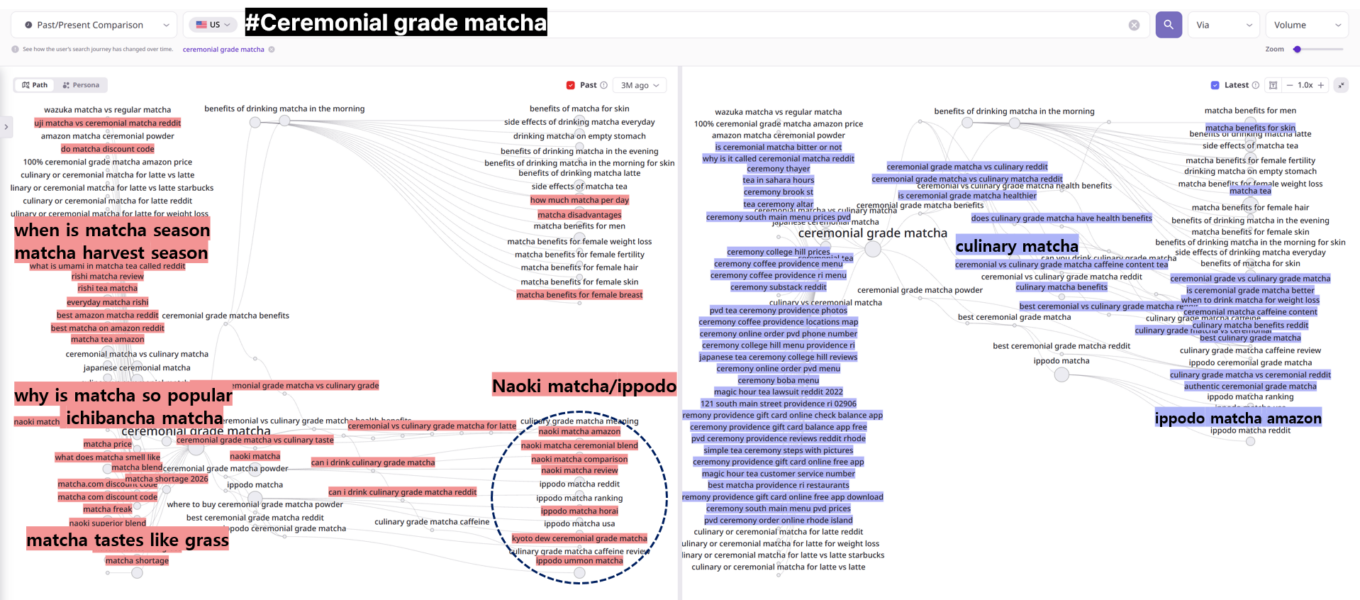

How Consumer Interest in Ceremonial Grade Matcha Has Shifted in 3 Months

Comparing ceremonial grade matcha search paths from three months ago to today, a clear behavioral shift emerges.

Disappeared paths (red): supply anxiety and early-stage curiosity fading out

Three months ago, search paths included early-stage discovery queries:

'when is matcha season

,

ichibancha matcha

,

why is matcha so popular'

, and ‘

matcha tastes like grass

‘. Heavy concentration around a single brand (

naoki matcha, ippodo

) also characterized this earlier period.

The disappearance of these paths suggests the market has moved through an “anxiety and discovery” phase and into something more settled.

Newly appeared paths (blue): comparison, brand selection, and real-world experience

The paths emerging now tell a different story.

'Culinary matcha'

appearing as a new path suggests that consumers who’ve discovered ceremonial grade are now circling back to evaluate culinary grade—a sign of a more sophisticated consumer, not a less interested one. ‘

Ceremonial grade vs culinary grade matcha'

reflects a consumer who knows what they’re looking for and is in the process of choosing. Also worth noting: ‘

ippodo matcha amazon'

is a new addition to the path—notable because interest in Ippodo itself has been present for months, but consumers are now moving from awareness to active purchase behavior via Amazon.

One-line summary: Ceremonial grade matcha search behavior has shifted from supply concerns and first-time curiosity toward grade comparison, brand evaluation, and café discovery—indicating a measurably more mature consumer base.

Explore the U.S. Matcha Market with ListeningMind

Taken together, the search data tells a coherent story. Matcha latte has established itself as the category’s entry point. Matcha powder holds the largest volume but is in a consolidation phase. And ceremonial grade matcha, after a near-vertical surge, is now emerging as the format of choice for the category’s most informed consumers.

What this signals at a market level: the reasons Americans are drinking matcha are changing. What started as a casual café trend is maturing into something more deliberate—a wellness habit shaped by grade awareness, sourcing preferences, and a growing familiarity with Japanese brands and standards. The data captures that evolution in real time.

ListeningMind is a market intelligence tool that analyzes U.S. search data across three dimensions: keyword volume and trend, topic clusters, and search path analysis. If you want to track how consumer interest in a category like matcha is shifting—by format, by intent, and over time—it’s built for exactly that.

FAQ

Based on data from June 2022 through May 2026, the U.S. matcha market spans more than 119,000 keywords, with a combined monthly search volume of approximately 7.9 million and an annual total exceeding 90 million searches. The top keywords include

matcha near me

(over 1,073,000 monthly searches) and

matcha

(882,000/month), reflecting both sustained category interest and a sharp rise in local, in-person discovery intent.

Path analysis data shows a clear behavioral shift over the past three months. Earlier search paths were concentrated around supply concerns (matcha shortage, tariffs on Japanese imports), brand-specific discount codes, and basic questions about taste and harvest seasonality. Current paths show increasing interest in culinary vs. ceremonial grade comparisons, specific brand selection (particularly Ippodo via Amazon). This shift suggests that ceremonial grade matcha buyers are moving from early-stage curiosity toward more deliberate, brand-informed purchasing.

Search data captures consumer intent at scale—before a purchase decision is made. Unlike sales data, it reveals what questions consumers are actually asking, which formats they’re comparing, and how their priorities are evolving. For the matcha market, this means identifying not just which products are growing, but why: whether demand is being driven by café culture, wellness routines, or a growing interest in quality and sourcing. It’s a leading indicator, not a lagging one.